When it comes to financing your education, understanding the differences between subsidized vs unsubsidized student loans is crucial. Both types of loans are part of the federal student loan program, designed to help students cover the costs of higher education. However, they have distinct features that can significantly impact your overall financial burden during and after your studies.

At Sadek Bankruptcy Law Offices, we are dedicated to helping students in Pennsylvania and New Jersey understand their loan options and provide them with personalized debt relief solutions. If you have already taken out a subsidized or unsubsidized loan for your education and are overwhelmed by student loan debt, contact a Philadelphia student loan debt relief attorney at Sadek Law today.

Together, we can help you explore your options and find the best path forward for your educational and financial future. Call our Pennsylvania number at (215) 545-0008 or our New Jersey number at (856) 890-9003 to schedule a free consultation with a member of our team regarding your situation.

What Is the Federal Direct Loan Program?

The William D. Ford Federal Direct Loan Program (also known as the Direct Loan Program) is a U.S. government initiative that provides low-interest student loans to help cover the cost of higher education. Unlike private loans, these loans are issued directly by the federal government through the Department of Education, and they come in various forms, including Direct Subsidized Loans and Direct Unsubsidized Loans.

This program offers flexible repayment options and is designed to make college more accessible to individuals with a greater financial need.

What Is FAFSA?

FAFSA, or the Free Application for Federal Student Aid, is an online form that students in the U.S. must fill out to apply for financial aid for college or graduate school. It helps determine a student’s eligibility for federal grants, loans, and work-study programs, as well as some state and institutional aid.

Once you apply for FAFSA, your school’s financial aid office will use the financial information you’ve provided to calculate how much aid you are eligible to receive based on your financial needs.

Federal Student Loans Qualifications

In order to determine which loan is right for you, it’s important to know which loan you actually qualify for. Below are the qualifying criteria for subsidized and unsubsidized loans.

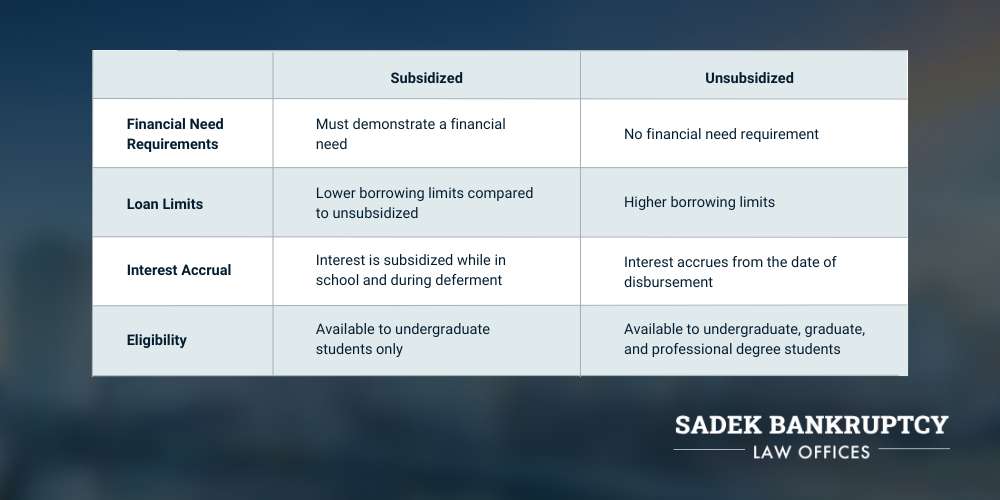

Subsidized loans require borrowers to demonstrate financial need, whereas unsubsidized loans do not have a financial need requirement. Additionally, the federal government pays the interest on subsidized loans while the borrower is in school or during deferment, while unsubsidized loans accrue interest from the moment they are disbursed.

Direct subsidized loans generally have lower borrowing limits compared to direct unsubsidized loans, which offer higher maximum limits. This allows unsubsidized loans to accommodate a broader range of educational expenses. Lastly, subsidized loans are only available to undergraduate students. In contrast, unsubsidized loans are available to undergraduate students, graduate students, and professional degree students.

What Are the Maximum Borrowing Limits for the Federal Direct Loan Program?

The Direct Loan Program sets annual and lifetime borrowing limits based on a student’s year in school and their dependency status. For dependent undergraduate students, the maximum annual loan limit ranges from $5,500 for first-year students to $7,500 for third-year students and beyond. Independent undergraduates can borrow more, with annual limits ranging from $9,500 to $12,500.

Graduate or professional student borrowers have a higher annual limit of $20,500 for unsubsidized loans. The total borrowing limit for undergraduates is $31,000 for dependents and $57,500 for independents, while graduate students can borrow up to $138,500. The graduate aggregate borrowing limit also includes any loans they received during their undergraduate career.

What Is the Difference Between Subsidized and Unsubsidized Loans?

When it comes to financing education, understanding the difference between subsidized vs unsubsidized student loans is essential for making informed decisions. Both types of loans are offered through the federal government, but they cater to different financial needs and circumstances.

Below we’ll explore each loan type in more detail, helping you determine which option may be right for you.

Subsidized Loans

First, we’re going to talk about subsidized student loans, their qualifying requirements, and their main advantage over unsubsidized student loans.

Direct Subsidized Loan

Direct subsidized loans are a type of federal student loan offered through the Direct Loan Program. These loans are only available to undergraduate students, and in order to qualify, you must demonstrate a financial need.

The main advantage of these loans is that the U.S. Department of Education covers the interest on the loan while you are enrolled in school at least half-time, during the six-month grace period after leaving school, and during your deferment period. This makes them more affordable than loans where interest accumulates immediately, like direct unsubsidized loans.

Do Subsidized Loans Have Interest?

Yes, subsidized loans do have interest, but the U.S. Department of Education covers it while the student is enrolled at least half-time, during the six-month grace period after leaving school, and during deferment periods.

Unsubsidized Loans

Next, we’re going to discuss unsubsidized federal student loans and how they compare to subsidized loans.

Direct Unsubsidized Loan

Direct unsubsidized loans are federal loans that are available to undergraduate, graduate, and professional students. Additionally, they can be granted to students regardless of their financial need.

Unlike subsidized loans, interest on unsubsidized loans starts accruing as soon as the loan is disbursed. These loans offer flexible repayment options but come with the added cost of accumulating interest throughout the borrowing period.

Do Unsubsidized Loans Have Interest?

Yes, unsubsidized loans have interest, and it begins accruing from the moment the loan is disbursed. Unlike subsidized loans, the government does not cover the interest at any point.

While students can defer interest payments while in school, any unpaid interest will capitalize, meaning it gets added to the principal balance, which increases the total amount that must be repaid over time.

Understanding Repayment of Subsidized and Unsubsidized Loans

The repayment period for subsidized and unsubsidized loans typically begins six months after graduation, leaving school, or dropping below half-time enrollment, also known as the grace period. For subsidized loans, the government covers the interest during this grace period, while for unsubsidized loans, interest begins accruing immediately, meaning borrowers may owe more once repayment starts.

Both types of loans offer several repayment plans, including standard, graduated, and income-driven options, allowing borrowers to choose a plan that best fits their financial situation. It’s crucial for borrowers to communicate with their loan servicer and stay informed about repayment options to manage their debt effectively and avoid potential default.

At Sadek Bankruptcy Law Offices, our experienced bankruptcy lawyers understand the challenges that come with repaying subsidized and unsubsidized student loans. If you’re struggling to meet your loan obligations, we can guide you through the options available to alleviate your financial burden.

Our team will assess your individual situation, providing personalized advice on whether bankruptcy might be a viable solution. While student loans are typically not dischargeable in bankruptcy, certain circumstances—such as proving undue hardship—can lead to relief.

We will help you explore income-driven repayment plans, loan consolidation, or deferment options to manage your payments more effectively. If bankruptcy is appropriate, our attorneys will work diligently to prepare and present your case, advocating for your best interests and aiming for the most favorable outcome possible.

What Are the Pros and Cons of Subsidized and Unsubsidized Student Loans?

Both subsidized and unsubsidized loans come with their own set of advantages and disadvantages. When deciding between the two, it’s important to weigh these pros and cons to find the loan that’s right for you. Below are the pros and cons of subsidized vs unsubsidized loans.

Pros of Subsidized and Unsubsidized Loans

Here are some key pros for each type of loan:

Pros of Subsidized Loans

- No interest accrual while in school, decreasing the overall cost of the loan.

- Lower interest rates compared to unsubsidized loans.

- Financial need requirements prevent borrowers from taking out federal student loans they don’t need.

Pros of Unsubsidized Loans

- No financial need requirements, which can make them more accessible to borrowers.

- Higher borrowing limits, which can allow students to borrow more each year.

- Flexible repayment options to choose from, including options that can accommodate various financial situations.

Cons of Subsidized and Unsubsidized Loans

In contrast, here are some of the cons of each type of loan:

Cons of Subsidized Loans

- Only undergraduate students with demonstrated financial need qualify, which may exclude some borrowers.

- Lower annual and lifetime borrowing limits compared to unsubsidized loans, which can potentially require additional borrowing.

- Interest rates can change, impacting the overall cost if rates increase during the loan term.

Cons of Unsubsidized Loans

- Interest begins accumulating immediately, which can lead to a larger total repayment amount over time.

- Higher interest rate costs compared to subsidized loans.

- Potential for debt accumulation due to ease of access, resulting in higher debt burdens.

In conclusion, understanding the potential upsides and downsides of both subsidized and unsubsidized loans is crucial for you as you plan your education financing. Evaluating these pros and cons can help you make informed decisions about which loan types best align with your financial situation and long-term goals.

Subsidized and Unsubsidized Loan FAQs

Which Loan Type Provides Interest Subsidy?

Subsidized loans provide you with an interest subsidy. With these loans, the U.S. Department of Education pays the interest while the student is enrolled at least half-time, during the six-month grace period after graduation, and during periods of deferment.

This feature helps reduce the overall cost of borrowing compared to unsubsidized loans, where interest accrues from the time the loan is disbursed.

Do You Have to Pay Back Unsubsidized Loans?

Yes, you do have to pay back unsubsidized loans. Borrowers are responsible for the entire amount borrowed, plus any interest that has accrued from the time the loan is disbursed. While students can choose to defer payments while in school, any unpaid interest will capitalize.

This means it gets added to the principal balance, which can increase the total amount owed over time. It’s important to understand the repayment terms and plan accordingly to manage this debt effectively.

When Do Unsubsidized Loans Accrue Interest?

Unsubsidized loans accrue interest from the moment they are disbursed. This means that interest begins accumulating immediately, regardless of whether the student is enrolled in school or in a deferment period.

Unlike subsidized loans, where the government covers interest while the student is in school, borrowers of unsubsidized loans are responsible for paying the student loan interest throughout the life of the loan, including during periods of enrollment.

Are Subsidized Loans Interest-Free?

No, subsidized loans are not interest-free. The student must make all remaining interest payments on their loan after they graduate, drop out, or are otherwise no longer enrolled in school at least half-time, after their six-month grace period after graduation is up, and/or after they are no longer in deferment.

While subsidized loans have lower costs during school, and they offer significant interest benefits, they do eventually incur interest once repayment begins.

Should I Pay Off Subsidized or Unsubsidized Loans First?

Generally, you should pay off unsubsidized loans first. Since unsubsidized loans accrue interest from the moment they are disbursed, they can become more expensive over time due to accumulating interest.

Paying off these loans first can help minimize overall interest costs. However, if you have a specific financial situation, such as income-driven repayment plans or forgiveness options, consider those factors in your decision.

Ultimately, prioritizing loans with the highest interest rates can be a sound strategy to reduce debt more effectively. At Sadek Bankruptcy Law Offices, we can evaluate your situation and advise you on the best course of action regarding your federal student loans.

Contact a Student Loan Bankruptcy Attorney in Pennsylvania and New Jersey at Sadek Law

If you’re struggling with your existing federal loans and considering your options for debt relief, contact the Pennsylvania and New Jersey attorneys at Sadek Bankruptcy Law Offices today. We understand that the burden of student loans can feel overwhelming, especially when you are trying to build a stable financial future.

Our experienced team is dedicated to helping our clients explore their rights and potential solutions for managing their student loan debt. Whether you are dealing with federal or private student loans, we can provide you with the legal options you need to seek relief from overwhelming debt and creditor harassment.

Student loan bankruptcy can be a viable option for those who qualify, but the process can be challenging without expert guidance. Our attorneys are well-versed in the nuances of student loan laws and can help you assess your situation to determine the best course of action. If you have questions about student loan debt relief or want to get started with us today, call our law firm to schedule a consultation with us.

Pennsylvania residents can call us at (215) 545-0008, and New Jersey residents can call us at (856) 890-9003. You can also contact us online via our website to schedule your free consultation with a debt relief attorney on our team.